| |

|

General Information |

|

Electric Vehicles in Asia Pacific

|

| |

| |

EVS |

| |

LINK |

|

| |

Events |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Korea Korea |

Home > Electric Vehicles in Asia Pacific > Korea |

| |

|

|

Electric Vehicle

(Development history)

In the early 1990s, the development of conversion cars and concept cars aimed at developing high-performance electric vehicles centered on automakers and laboratories was active in Korea in line with the global electric vehicle development boom, but none of them actually led to practical use.

However, in October 2009, the government announced plans to revitalize the electric vehicle industry as a policy to enter the four largest green cars country in 2013, and the movement to make electric vehicles more practical gradually began. Since then, development of electric vehicles has been carried out in two major directions: low-speed electric vehicles and high-speed electric vehicles.

The start of the low-speed electric vehicle(LEV) was vehicle for short-distance driving with a maximum speed of 60 km/h and a total weight of 1,361 kg. It was developed and sold by small and medium companies in the second half of 2009, but sales were very low due to low safety and high cost. Although laws and regulations for driving such as designation of low-speed electric vehicles and driving zones, road sign design, and safety standards have been completed in March 30, 2010, but few have remained due to the bankruptcy of companies.

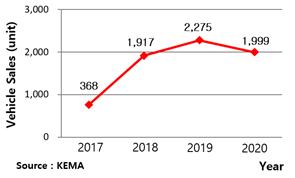

In July 2018, ultra-small electric vehicles, such as the Twizy, were introduced in Europe in the L7e category. Ultra-small electric vehicles are max. 3.6 m length, max. 1.5 m width, max. 2.0 m height, max. speed 80 km/h, max. power 15 kW, max. weight 600 kg (passenger car), and 750 kg (cargo) and separate safety standard has been established for existing electric vehicles. And the Korea Post has been purchasing 1,000 ultra-small electric cargo vehicles and is currently forming a market of 2,000 vehicles annually.

|

|

|

| <Ultra small electric vehicle sales per year in Korea> |

|

|

|

| Renault Samsung TWIZY |

CAMMSYS CEVO-C |

MASTA VAN |

|

| <Ultra small electric vehicle in Korea> |

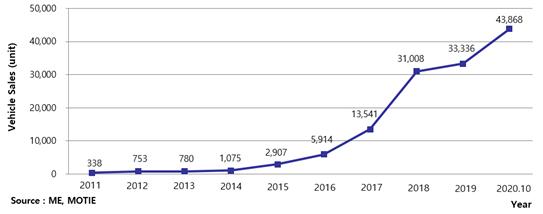

For high-speed electric vehicles, Hyundai Blue-on electric vehicles were developed in August 2010, producing 250 units for public organizations, which were announced as the main model of the government demonstration project. Since then, first-generation electric vehicles such as Renault Samsung SM3 EV, GM Korea SPARK EV and BMW i3 have been on the market, but no significant expansion has been made due to short driving range per one charge, lack of charging facilities and social atmosphere. However, after second-generation electric vehicles like GM Korea's BOLT EV and Tesla's Model 3, which have a driving range per one charge more than 300 km, were released in 2017, sales of electric vehicles have increased rapidly. In particular, Hyundai Ionic 5 is introducing a feature that allows the electrical energy of the traction battery in the vehicle to be used at 220 V power through the Vehicle to Load (V2L) function, which is a new attempt to utilize electric vehicles.

|

|

|

| <Electric vehicle sales per year in Korea> |

|

|

|

| GMKorea BOLT EV |

Kia NIRO EV |

Hyundai IONIQ 5 |

|

| <Electric vehicle in Korea> |

(Policy Support)

Korea's electric vehicle policy is in charge of 3 ministries – the MOTIE(Ministry of Trade, Industry and Energy) for technology development of vehicle and auto parts, the ME(Ministry of Environment) for propagation of electric vehicle and infrastructure and the MOLIT(Ministry of Land, Infrastructure and Transport) for safety certification. Previously, separate support measures were prepared for each ministry's responsibility.

However, as an action plan to create a new energy industry to cope with climate change crisis announced in July 2014, comprehensive support measures were prepared to supply 200,000 electric vehicles under the "Plan to expand the supply of electric vehicles and revitalize the market" jointly announced in December 2014.

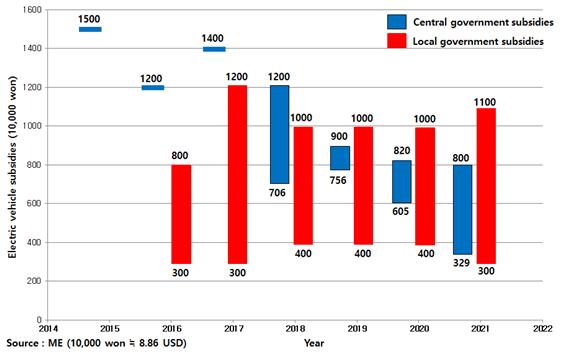

The most important subsidies for expanding the supply of electric vehicles are budgeted by the ME, and as of 2021, the central government subsidies are 3.25 to 8 million won depending on vehicle types and the local government subsidies are 3 to 10 million won, but subsidies are decreasing every year. As of 2021, 65 electric vehicles, including Hyundai Ionic 5, Renault Samsung ZOE, 28 electric cargo vehicles, including Kia Bongo III electric vehicles, and 67 electric buses are aimed as target of 121,000 electric vehicles.

In addition, initial government support was focused on purchase subsidies, but it has recently been supported in various areas, including discounts on public parking fees and charging fees, and support for installation of public chargers. In particular, the government is enforcing a mandatory blue license plate (excluding business use) for newly registered electric vehicles and fuel cell electric vehicles to more easily provide discounts such as parking fees and tolls since June, 2017.

|

|

|

| <Central and local government subsidies for electric vehicle in Korea> |

(Charging Infrastructure)

The most urgent works for the expansion of electric vehicles is the establishment of charging infrastructure. Charging infrastructure can be divided into rapid charging station, slow charging stand and mobile charger.

|

|

|

<Three types of electric vehicle charging infrastructure>

|

Since most residents in Korea live in public building such as apartments, it was very difficult to set up parking lots exclusively for electric vehicles in existing apartments. In order to solve the electric vehicle charging problem of apartments, the government pushed for the introduction of a 'mobile charger' system. In a press release dated May 8, 2017, the MOLIT announced that parking lots for more than one-fifty of the number of new apartments to be built will be mandatory for portable chargers for electric vehicles. This method carries a charger with a built-in cable meter in the vehicle without installing a charger, utilizes an outlet (220 V) installed in an apartment house or building, and uses RFID tags attached to separate the electric bill from existing facilities.

In August 2016, the MOLIT and the KEPCO(Korea Electric Power Corporation) announced plans to build a total of 200 billion won worth of charging infrastructure for electric vehicles for the expansion of rapid and slow charging infrastructure. As of the end of November 2020, total 62,789 accumulated public chargers with 9,661 rapid and 53,128 slow chargers have been built, and 134,430 electric vehicles are propagated. This is similar to the installation of one charger per two electric vehicles.

|

| Electric vehicle charging infrastructures in Korea |

| Charging type |

~’18 |

2019 |

2020.11 |

Total |

| Total |

27,352 |

17,440 |

17,997 |

62,789 |

| Rapid |

5,213 |

2,183 |

2,265 |

9,661 |

| Slow |

22,139 |

15,257 |

15,732 |

53,128 |

|

Since the second half of 2014, domestic rapid charging stations have been installed with complex multi-types that support both CHAdeMO, AC3 phase, and Combo 1. But the need for standardization has been continuously required, so the rapid charging method was unified into Combo 1 by the KATS(Korea Agency for Technology and Standards) in December 2017.

In addition, for the convenience of electric vehicle charger users, the government has prepared a policy to jointly use chargers from eight charging businesses with one member card since October 2018, and provides easy finding of electric vehicle charging stations through the low pollution vehicle integrated guide homepage (www.ev.or.kr). In particular, the ME announced that it will be built more than 70 units of 350 kW ultra rapid chargers suitable for electric vehicles with increasing battery capacity in public-private partnerships at major highway rest areas across the country starting in 2021.

|

|

|

<350 kW ultra rapid charging station>

|

| <Vehicle charging connectors and vehicle sockets used in Korea> |

| Type |

AC single phase

5 pins(slow) |

AC 3phase 7 pins

(rapid/slow) |

DC CHAdeMO

10 pins(rapid) |

DC combo

7 pins(rapid) |

Charging

connector |

|

|

|

|

Vehicle

socket |

|

|

|

|

|

(Future Outlook)

In February 2021, the government announced “the fourth basic plan for eco-friendly cars”, setting a target of eco-friendly cars support of 2.83 million by 2025 and 7.85 million by 2030. It is also planning to support the construction of chargers with more than 50% of the number of electric vehicles and supply ultra rapid chargers that can supply energy to electric vehicle for travel 300 km with a 20-minute charge.

|

| <Rapid charging stations> |

| Power |

50kW |

100kW |

200kW |

350kW Ultra rapid |

| Shape |

|

|

|

|

| Connector |

AC 3 phase, DC CHAdeMO, DC combo |

DC combo |

DC combo(concurrent charging) |

DC combo(water cooling) |

| Charging time |

80~90 min. |

55~60 min. |

30~35 min. |

about 20 min. |

|

| <Slow charging stands and mounts> |

| Type |

Independent(Stand, Wall mounting) type |

Socket type |

Streetlight type |

| Shape |

|

|

|

| Shape |

7 kw |

3 kw |

3~7 kw |

| Charging time |

7~8 hours |

14~17 hours |

7~17 hours |

|

| <Electric vehicle charging station (www.ev.or.kr)> |

|

|

|

|

|

|

|

EVAAP

EVAAP China

China Hong Kong

Hong Kong Japan

Japan Korea

Korea